Impact windows insurance discounts in Florida typically range from 15 to 45 percent, depending on your home’s protection level and inspection rating.

Florida homeowners’ insurance rates have climbed sharply in recent years, especially along the Gulf Coast. For homeowners in Sarasota, Bradenton, and surrounding areas, this is one of the few upgrades that can directly reduce ongoing insurance costs, not just improve protection.

Quick Answer:

Insurance companies price your policy based on how likely your home is to sustain damage during a storm. Homes with unprotected openings are far more vulnerable to internal damage when windows fail under pressure.

Impact windows are designed to resist both debris impact and wind pressure, helping prevent that failure. When this protection is verified, insurers classify the home as lower risk, which is what triggers the discount.

Impact windows are designed to stay intact under high wind loads and debris impact. They prevent the building envelope from being breached during a storm. That directly reduces the insurer’s exposure and earns you a wind mitigation credit on your policy.

The discount applies to the windstorm portion of your premium, not the full bill. In coastal counties, windstorm coverage often makes up 50 to 60 percent of the total premium, so the savings are still significant. Homeowners with a fully protected home (every window, door, and skylight is impact-rated) qualify for the highest available opening protection rating, which unlocks the maximum credit.

Discounts vary by location and insurer. In Sarasota and Manatee counties, current premiums are often higher than historical averages, making the potential savings from impact windows more significant.

County | Avg. Annual Premium* | Windstorm Discount | Est. Annual Savings |

Miami-Dade | $6,000–$10,000+ | 25–45% | $1,500–$4,500+ |

Sarasota | $5,000–$8,000 | 15–30% | $750–$2,400 |

Manatee (Bradenton) | $4,500–$7,500 | 15–30% | $450–$1,650 |

Lee County (Fort Myers) | $4,000–$7,000 | 20–35% | $675–$2,250 |

Charlotte County | $3,500–$6,000 | 15–30% | $525–$1,800 |

Collier County (Naples) | $4,500–$8,000 | 20–35% | $900–$2,800 |

There are a few situations where you won’t see a full discount:

• Partial protection: If even one opening, such as a garage door, a skylight, or an old entry door, isn’t impact-rated, your opening protection rating drops. The discount shrinks or disappears.

• No inspection: Installing impact windows doesn’t automatically trigger a discount. You need a completed wind mitigation inspection and the OIR-B1-1802 form on file with your insurer.

• Older installations: Some insurers reduce credits for windows installed before the current Florida Product Approval standards were in place.

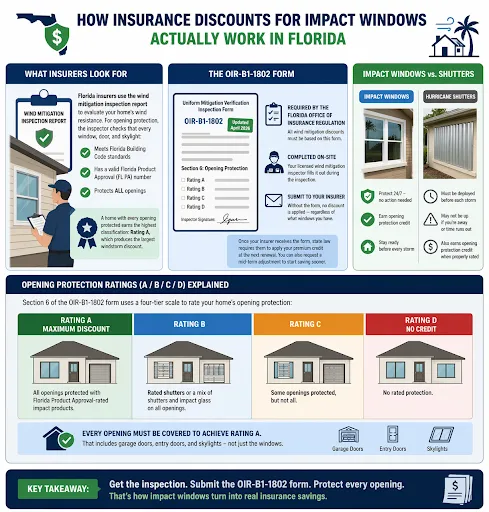

Florida insurers use the wind mitigation inspection report to evaluate your home’s wind resistance. For opening protection, the inspector checks whether every window, door, and skylight is rated to Florida Building Code standards and carries a valid Florida Product Approval (FL PA) number. A home with every opening protected earns the highest classification Rating A, which produces the largest windstorm discount.

The Florida Office of Insurance Regulation requires all wind mitigation discounts to be based on the Uniform Mitigation Verification Inspection Form (OIR-B1-1802). The form was updated in April 2026 for improved accuracy, but the process is unchanged — your licensed wind mitigation inspector completes it on-site, and you submit it to your insurer. Without it, no discount is applied, regardless of what windows you have.

Once your insurer receives the form, they’re required by state law to apply a premium credit at your next renewal. You can also request a mid-term adjustment to start saving sooner.

Both impact windows and rated hurricane shutters can earn opening protection credits. The key difference is that shutters must be deployed before each storm. If a homeowner is away or the storm arrives quickly, shutters may not be up. Impact windows protect the home at all times; no action required. For a side-by-side breakdown, see hurricane shutters vs. impact windows.

Section 6 of the OIR-B1-1802 form rates your home’s opening protection on a four-tier scale:

Every opening in the home must be covered to achieve Rating A. That includes garage doors, entry doors, and skylights, not just the windows.

A licensed wind mitigation inspector visits your home and completes the OIR-B1-1802 form. For opening protection, they verify the FL PA numbers on your windows and doors, confirm every opening is covered, and assign a rating. They also document your roof shape, deck attachment, and wall connections since the roof factors into the overall credit calculation. The visit typically takes 45 to 90 minutes.

Wind mitigation inspections typically cost between $75 and $200. You can find licensed inspectors through your insurer, your contractor, or online directories. Given that the inspection can save you hundreds of dollars per year, it pays for itself quickly.

Once the inspection is done, the inspector gives you the completed OIR-B1-1802 form — usually within a few business days. Submit it directly to your insurance agent or carrier. Most insurers process it within 30 days. Keep a copy. The report is valid as long as your protection remains in place, and most insurers accept reports up to five years old.

The OIR-B1-1802 form documents nine features of your home: building code compliance, roof covering, roof deck attachment, roof-to-wall connection, roof shape, secondary water resistance, and opening protection. Each one affects your wind mitigation credit. The form creates a standardized record that any Florida insurer can use to calculate your discount.

Florida law requires insurers to offer wind mitigation credits, but only based on verified documentation. The OIR-B1-1802 is that documentation. Without it, your insurer can’t adjust your premium, even if they can see impact windows on your home.

Impact windows with a valid FL PA number are what earn a Rating A on Section 6 of the form. That’s the opening protection section and the one that drives the windstorm discount. For more on what separates impact glass from standard windows, see standard vs. impact windows.

A homeowner in Bradenton with a 2,200-square-foot home built in the late 1990s had no rated opening protection, per the inspection form. Annual homeowners insurance, including windstorm coverage, was approximately $5,000.

After replacing all windows and entry doors with Florida-certified impact products and completing a wind mitigation inspection, the homeowner submitted the OIR-B1-1802 form to their carrier. Combined with an existing hip roof, the opening protection upgrade earned a 28 percent windstorm credit.

Windstorm coverage made up roughly 60 percent of the total premium. A 28 percent credit on that portion translated to about $840 in annual savings. Over ten years, that’s more than $8,000 before factoring in energy savings or increased resale value. For a longer-term breakdown, see long-term savings of storm-proof windows.

Florida’s My Safe Florida Home grant program offers income-qualified homeowners a dollar-for-dollar match on hurricane-hardening upgrades, including impact windows up to $10,000. The program is administered by the Florida Department of Financial Services and requires a state-approved inspection before work begins. Funding is subject to availability, so checking early in the year is advisable.

Under the Inflation Reduction Act, homeowners may qualify for a federal tax credit on windows that meet Energy Star’s Most Efficient criteria. The credit applies to product cost, not installation, and is capped annually. Not all impact windows qualify. Ask your contractor to confirm Energy Star certification on the specific product before assuming eligibility.

Florida exempts impact-resistant windows and doors from sales tax at the point of purchase. This reduces your upfront cost automatically, no application required.

Impact windows are a valued feature in the Southwest Florida real estate market. Buyers understand the difference between a home that’s hurricane-ready and one that isn’t, and they’ll pay for it. Combined with insurance savings and energy efficiency, the upgrade is one of the strongest financial cases you can make for a home exterior improvement on the Gulf Coast.

Florida has no state income tax, so there’s no Florida-specific income tax credit. However, the federal Inflation Reduction Act’s energy-efficiency credits apply to Florida homeowners, provided the windows meet Energy Star thresholds. The Florida sales tax exemption on impact-rated products applies to everyone, regardless of income.

Every impact window and door installed in Florida must carry a Florida Product Approval (FL PA) number from the Florida Building Commission. This confirms the product has been tested to meet Florida Building Code wind load and impact resistance standards. Your contractor should provide the FL PA number for each product, and that number should appear on your permit documents. Without it, your inspector can’t assign a Rating A, and no maximum discount follows.

Homes in Miami-Dade and Broward counties must use products that also carry a Miami-Dade Notice of Acceptance (NOA). This is a stricter certification developed after Hurricane Andrew for the High-Velocity Hurricane Zone (HVHZ). If your home is in one of these counties, confirm that your contractor specifies products with both Florida Product Approval and a current Miami-Dade NOA.

A certified product installed incorrectly won’t perform to its rated specifications. Improper anchoring, missing flashing, or gaps in installation can cause failure during storms. For insurance purposes, it also needs to be permitted. Permitted work creates the documentation trail wind mitigation inspectors rely on to verify compliance. Unpermitted installations can disqualify you from a Rating A and create complications with claims later. See impact windows in Sarasota and Bradenton for what a proper installation looks like.